Electricity as fuel: the crossover moment (Batteries Part I)

Blog_7

I was scrolling through Twitter the other day and came across a Tweet that made me stop and think for several minutes.

At first, this seemed like an obvious statement — plenty of cars run on electricity, obviously electricity is a kind of fuel in that context. The issue, I naively thought, was that electricity needs to be generated by something, and in today’s world the generative input can be anything from solar and wind to coal or natural gas. But as I pondered for several more minutes, I realized that the existence of an underlying non-electric energy source is not strictly necessary for the generation of electricity. I had been envisioning a hypothetical world where we did not already produce electricity and would need some external catalyst to get the closed system going. But this hypothetical was just that, a hypothetical, because electricity already exists and could absolutely be harnessed to generate more electricity — electricity as fuel.

The economic implications of electricity as fuel are pretty massive: transportation, home and commercial energy supply, energy grids, and more could all move off of legacy fuels, thereby spurring large investments in energy storage technology and a wholesale reimagining of how we power our lives. This evolution won’t happen without battery technology, including existing Lithium-ion batteries and nascent technology with applications beyond light automotive transportation. While I have much to share on the technology and markets around batteries, allow me a brief digression to address a material geopolitical reality that has been illuminated by the ascendance of batteries. From a Wall Street Journal article (linked here), “nearly 65% of lithium-ion batteries come from China. By comparison, no single country produces more than 20% of global crude oil output.” That is supply concentration like the world has never seen, and it involves what is undoubtedly a crucial input into energy production in what must be a less carbon-intensive future.

It seems like a legitimate economic and national security concern for the United States that the path to emissions-free energy production runs through a country with which the US has an adversarial relationship in good times. If we thought oil conflict in the Middle East and resulting domestic economic impacts were bad, just wait for the battery conflicts. I believe that at a certain point domestic battery production will become an issue of national security, in much the same way semiconductors have become a geopolitical and economic flashpoint between the US and China over the last 10 years.

The US could address this threat head-on and in relatively early innings by decreasing supply exposure to China and diversifying to non-Li-ion battery types (the latter of which is likely to happen anyway as many heavier applications won’t rely on Lithium; will touch on this later). The upside to bringing battery production back home is American jobs, and lots of them. There’s always been this narrative in the popular discourse that solving global warming necessarily implies cutting back, reducing consumption, or otherwise sacrificing economic output to reduce emissions. This is a false narrative. Solving climate change will require a gradual but wholesale reimagining of society and our economy, and while that will certainly mean the end of some industries in the medium to long term, it does not mean a net job loss. As I’ve written before here, there are many skills from legacy energy sectors that are highly applicable to emerging sectors. Moreover, for those industries where a job transition is less obvious, a revitalization of the American workforce impacted by job loss on the government’s dime (read: our dime) would be a sensible investment in US national security, energy independence, and economic power. Beyond both of those things, the potential for future GDP growth on the back of cheap, domestically produced renewable energy powering reimagined manufacturing, supply chain, transportation, and agriculture businesses is really exciting — it’s a chance to rebuild America for the 21st century and onward. (End rant, on to batteries.)

To transition to electricity as fuel, growing battery adoption will be key. I didn’t (and still don’t, to be perfectly honest) have a particularly sophisticated grasp of battery chemistry, so I had to do some reading to get up to speed. For those who similarly don’t know much about batteries, hopefully this overview is helpful. Batteries have 3 main components: two electrodes, one positively charged and one negatively charged, and an electrolyte substance that separates the two. Inside the battery, a chemical reaction occurs, producing positively charged ions and negatively charged electrons. These negatively charged electrons flow through a circuit external to the battery, and this flow generates an electric charge, or electricity. In rechargeable batteries, which are for the most part the only kind that will be useful in the applications I discuss here, the chemical reaction that causes the electron flow is reversible. During charge, positively charged Lithium ions move from the positive electrode to the negative electrode. When the battery discharges, the ions fall back to the positive electrode as electrons cycle back to the negative electrode, and this process generates electricity.

Some other definitions will be helpful before I dive into the next bit:

- Energy density is the amount of energy in a system per unit of system volume. Higher energy density means more energy per unit of volume, or same energy across smaller volume. This is important for transportation battery applications.

- Cycle life is the number of full discharge cycles it takes to reduce a battery’s capacity to a pre-determined fraction of its original capacity (i.e. # of full discharge cycles it takes to reduce a laptop battery to 80% of original capacity). Longer cycle life means lower battery costs overall.

According to Tesla’s Battery Day 2020 presentation, one of the biggest challenges facing automotive applications of batteries is the tradeoff between energy density and battery life span, or in other words, developing a battery with the most energy per unit of volume that will also last a really long time. This is a central tradeoff in the world of batteries, and Li-ion technology to date has offered the most optimal combination of these characteristics. This is what Tesla has focused on, and breakthroughs in this space continue — Tesla even has plans to vertically integrate and bring battery manufacturing in-house. One reason for this is to implement plans for a completely new configuration for its car batteries called the tab-less jellyroll cell (for which they have applied for a patent here). Tesla claims the tab-less technology will make manufacturing cheaper and easier while reducing ohmic resistance and heat generated within the battery, both of which lengthen the life of each battery cell — an improvement for one side of the central tradeoff that does not impact the energy density.

There are plenty of other battery developments outside of Tesla, and as I was researching for this piece I came across an incredible report from the Rocky Mountain Institute, linked here, which broadened my understanding of what batteries, including and beyond Li-ion, could be used for. I highly recommend anyone interested in the market opportunities ahead in energy storage, transportation, shipping, aviation, and more check it out. Here were my big takeaways from the report:

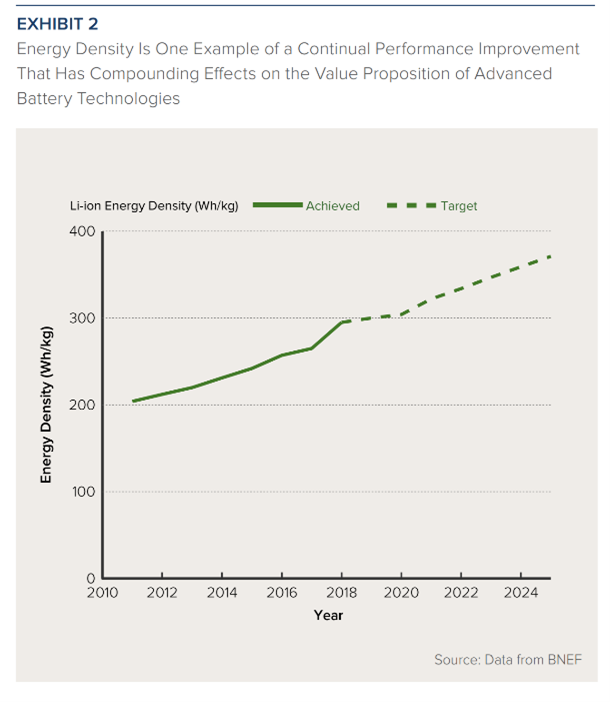

#1 Prices for Li-ion batteries are falling fast, and these price declines will drive greater investment in battery manufacturing capacity. Increased investment over the last decade has already produced improved batteries with higher energy density and longer lives. Energy density is the true competitive advantage when it comes to transportation applications, since more energy dense batteries can generate the same energy output with less weight; this has a compounding effect in the context of a car or truck, since it lessens the overall weight of the vehicle the battery has to power. To the left, historical and projected improvements in energy density suggest the potential for densities in the range of 375 Wh/kg, nearly doubling in 15 years. Improvements on this front will further lower the costs of battery-powered cars and other light transportation vehicles, driving adoption in the US and in less wealthy countries.

#2 Falling costs and growing Li-ion battery adoption are paving the way for investments in non-Li-ion battery alternatives. Since 2010, battery prices have fallen at an average annual rate of 21% while manufacturing capacity has exploded to meet rising demand in the US, Western Europe, India and China. As demand expands, costs of battery development will continue to fall, opening the door to non-Li-ion battery technologies becoming cost competitive and greater diversification of Li-ion applications. Increasing market options and thus more competitiveness will further reduce prices and drive even greater uptake, especially in industries previously untouched by the battery market due to pricing.

#3 Markets that have yet to be majorly disrupted by battery technology likely won’t rely wholly on existing Li-ion technology. Specifically, energy storage and heavy transportation like aviation and shipping will require more frontier technologies separate from or integrated with existing Li-ion batteries. An example is solid-state battery technology, which offers longer battery life, less sensitivity to temperature, and higher energy density and could be integrated into existing Li-ion manufacturing processes to produce higher-performing, though more expensive, Li-ion batteries. These characteristics make solid-state extremely amenable to wide-ranging applications in transportation, specifically in aviation where temperature controls are essential. The key challenge will be finding a battery that is powerful enough to fly the vehicle while not being absurdly heavy. Right now, short-haul flights of less than 3 hours are the most likely to be electrified. Converting these planes to battery power could materially impact aviation emissions, since short-haul flights like this account for 75% of flights taken globally.

Another very different market for new battery technology is long-duration energy storage of the type that will be needed in every energy grid facility in the US for widespread adoption of renewable energy in commercial and home settings. In 2018, demand for long-term storage was 20 GWh; this is projected to almost double year-on-year through 2030 as fossil fuels are increasingly replaced by renewables and battery support for the grid becomes required infrastructure. The batteries best-suited for this type of application have ultra-long lifetimes and are not built for power and as a result tend to be cheaper. The previously referenced WSJ article pointed out that even recycled Li-ion batteries from cars could be used as storage batteries, since they still hold charge but don’t offer the same power. As renewable energy continues to gain grid share, widespread deployment of battery storage will become an increasingly important element of energy delivery.

Overall, this report further cemented my longstanding view that systems approaches to climate change have the highest chances of success. On the technology and business side, Li-ion batteries are not a silver bullet to clean electrification of our lives, and electric cars are absolutely necessary but certainly not sufficient to solve the problem. Investors who identify businesses being built around many different battery applications including transportation, long-term storage, distributed charging networks, and the more ambitious applications of aviation and other heavy transport will build portfolios with higher chances of generating outsize returns. This feels especially true in aviation, where barriers to entry are high and a single company with sufficiently advanced battery technology could strike agreements with Boeing and Airbus early and completely dominate the global market for batteries supporting short-haul flights. Another interesting observation that I made while researching this piece is what Tesla is doing to vertically integrate the battery supply chain, and I wonder where else that may start to occur. For example, as grids increasingly need battery storage, public utilities may start buying up long-term battery storage companies. Another example, one that I think is likely, Boeing and Airbus could follow Tesla’s lead and bring battery production in-house through acquisition.

It’s clear that the future of energy will heavily rely on batteries for storage and deployment, and there are geopolitical and economic risks to not developing independent, domestic suppliers. Investment in the space is accelerating, and as a result Li-ion battery adoption is growing as costs are driven down. More frontier investments are also taking shape, and these technologies will be key to reinventing our energy grid, shipping and transportation, aviation, and more. Given all this, I am hoping to dig deeper into long-term storage applications and distributed charging networks. My next piece will be all about that so if you know of any good resources on the subject please send my way.