Guide to the Grid: Level 1

Blog_10

There’s a famous essay by David Foster Wallace called This is Water I once gave to a close friend for his college graduation. The essay in its entirety is rather profound, but the opening lines are lighthearted and relate closely to the topic I will cover in this post. Here is the opener:

“There are these two young fish swimming along, and they happen to meet an older fish swimming the other way, who nods at them and says, “Morning, boys, how’s the water?” And the two young fish swim on for a bit, and then eventually one of them looks over at the other and goes, “What the hell is water?””[1]

Before these last few weeks of research, I was the young fish swimming, oblivious to the water around me. In this analogy, the water I was completely unaware of is electricity and the electric grid through which it is distributed. Often, the most fundamental things in life are so ubiquitous that we fail to notice their existence and the massive impact they have on our lives. I am now older and wiser and want to share with other young fish the incredible complexity that is the electric grid as well as some areas I think are ripe for disruption. I would be remiss if I did not give a big shoutout to the FERC Energy Primer, which provided tons of helpful details and more information about the grid than I could possibly ever have imagined as I wrote this piece.

What the hell is water?

For those interested in a history of the electric grid and how it came to be today, I highly recommend reading The Grid: The Fraying Wires Between Americans and Our Energy Future by Gretchen Bakke, PhD. I am going to skip the history of the grid for now and focus on how it is set up, the different market participants, and how it all works together.

So, onward to the grid. It all starts from electricity, or the flow of electrical charge. Electricity is useful only insofar as our ability to channel it to the right sinks, where it powers everything from toaster ovens to office lights to surgical equipment and more. The entity that makes the movement of electricity possible is the grid, which generates, transmits, and distributes electricity. In the most abstract sense, the grid matches supply to demand in real time. In concrete terms, a grid is comprised of three main components — generation plants or assets, transmission assets, and distribution assets. Generation is what it sounds like. Natural gas or coal-fired power plants, solar or wind farms, hydropower, nuclear, or any other energy-generating asset (heck, even electricity itself can generate electricity, which I discuss here) are activated and produce energy which generates electricity; the electricity gets converted into super high voltages by a transformer and travels along long-distance transmission lines across entire states or regions (I will go into details further in this piece about how the grid is broken up).

Once transmission lines approach sources of demand, like the business or home for which the electricity is bound, the electricity passes through another transformer and ratchets down to a lower voltage. Now the electricity is ready for the distribution phase, the final step on the grid that delivers electricity to end users like you and me. The lower voltage electricity hits distribution lines (generally the powerlines you and I see walking around our neighborhoods) that then deliver that power to an electric socket or other endpoints near you. (Thanks to this amazing primer that sketched everything out for me).

Supply and Demand

The grid exists to generate and transport supply of electricity to sources of demand. Electricity can be supplied by any energy generating asset, such as the previously mentioned solar and wind, natural gas, coal nuclear, etc. Generation is usually the most expensive component of electricity supply, since the transmission and distribution lines and other maintenance costs are fixed costs spread across lots of paying end users and decades of service. Generation, by contrast, usually requires major capital investments up front that can take a long time to pay off. However, different types of generating assets supply electricity at different total costs (i.e. outside of infrastructure spend, wind and solar are free) and that makes a huge difference in the cost of energy. For example, parts of Texas saw negative electricity prices in 2015 as wind turbines generated more electricity than was demanded at the time (it was the middle of the night). Why couldn’t they just store all of the electricity produced in excess of the quantity demanded at the time? Because plants have to be sure to match electricity supply and demand every minute of every day of every year. This is a unique aspect of the electricity market — if supply and demand are not matched contemporaneously, the produced electricity is wasted. The only way around this is through large-scale battery storage (which I cover here), which can absorb and store the surplus electricity for later discharge to the grid. I’ll return to the need for utility-scale energy storage in the Grid Innovation section of this piece.

The demand side of the electricity market comes from a mixture of residential, commercial, and industrial customers, all of which have varying demand patterns and thus impact prices differently. Electricity demand curves are a function of many things, including season, weather, time of day, location, and more; in general, as demand rises, prices rise, to compensate for the fact that more expensive electricity generation sources have to fire up to meet demand. Interestingly, most consumers have price inelastic demand (meaning the demand curve does not shift up or down meaningfully based on the price of the electricity supplied) because most consumers are not able to see real-time price data for the electricity they consume and thus have no reason to shift their demand independently. Additionally, electricity is such a given in our lives that most people wouldn’t think twice about turning on the lights or the heat if they wanted to, regardless of price, which entrenches the price inelasticity of electricity demand. This is different than, for example, gas prices, because consumers can see prices rise week to week and choose to drive more or less in response. On the grid, demand is there no matter the price of electricity and the relatively inelastic demand with respect to price means supply is the only real lever that can be pulled to move the price, though there are some demand response programs which I will dive into shortly.

Within customer types, residential customers comprise ~37% of total capacity demanded. They have highly variable load shape, meaning the electricity demanded by a residential consumer at a given time fluctuates wildly; this demand variability makes it more challenging to predict and lock in supply to meet it and as a result residential prices tend to be high (though more extensive infrastructure like distribution lines to individual homes in remote locations also plays a role here). Commercial (~37%) and industrial (~26%) tend to pay lower rates since their load shape is much more predictable.

Managing the grid

The grid is a massive, interconnected system with lots of moving parts, which complicates the task of matching supply and demand across every hour of every day of ever year. Understanding ahead of time what demand might seems useful, and in its current state this practice is called load forecasting. Load forecasting is rigorous mathematical modelling that tries to predict electricity demand in order to more accurately match supply and demand on the grid. This is important because if there’s a mismatch, someone somewhere will not have power when they need it, which undermines everyday users’ trust in the system and negatively impacts the economy (the Department of Energy estimates power outages cost the US ~$150B per year). Load forecasting applies to three different time horizons:

- Short term: forecasts 1 hour — 1 week in advance and estimates the amount of electricity flowing through transmission equipment at a given time to prevent overload, thereby increasing grid reliability and reducing the chances of a blackout.

- Medium-term: forecasts1 week — 1 year in advance and estimates future demand to help plan new infrastructure and determine whether it will be sufficient to meet demand.

- Long-term: 1 year+; similar to medium-term forecasting, estimates future load demand to test whether infrastructure plans will be sufficient for expected future demand.

Having accurate forecasting models is a huge deal, and when they go wrong the price for electricity can skyrocket (if demand is higher than predicted) or the transmission lines can get overwhelmed and cause a blackout. This is an area where I think there AI could be hugely impactful and narrow the error bands on current forecasting models. Going forward, I hope to research this more here and learn about companies developing this technology (if you know of any please reach out!)

Aside from predicting demand, there are other demand response programs that can be implemented to help modulate demand in the short term. These programs incentivize consumers to shift their energy consumption outside of peak hours by, usually, offering slightly lower electricity prices during those times. The most extreme, curtailing, is common in Southern California during the hottest months of summer when demand spikes due to electricity usage (typically blasting the AC). County and city governments, in partnership with the electricity provider, request the public to limit their use of the AC, keep lights off, and generally reduce consumption to avoid overburdening the system. When this does not sufficiently reduce demand load, sometimes rolling blackouts are the only thing standing between consumers and a full-on blackout that can take days or weeks for the grid to recover from.

Shifting is another demand response program with more transparent remunerative benefits. In shifting, utilities offer consumers the option to agree to conducting certain activities, like laundry, lawn mowing, or other electricity-intense endeavors during lower-demand times of the day or week in exchange for lower energy rates. I think this is a particularly interesting in light of the emergence of the Internet of Things and connected, smart homes. In theory, if dishwashers and washing machines and refrigerators and AC and home charging ports were all connected to the grid in a smart way, they could automatically shift their electricity usage to off-peak-demand times of the day or week in order to minimize the cost of electricity (subject to constraints the consumer can control, for example, car must be charged by 7:45am every day to allow for a commute to work). And if many or most homes follow this protocol, the ease of load forecasting increases immensely since the impacts of shifting done by connected homes would be well defined beforehand. It’s almost like a network effect between load forecasting and shifting demand via connected, smart homes.

The final demand response program is onsite generation, in which a consumer takes him or herself off the grid completely and generates all power needed for day-to-day activities from an at-home energy source — be is solar panels, a generator, or something else. What if onsite generation results in a surplus of electricity above and beyond what a household demands? In some cases, the owner of the generating asset can start net metering, in which the generating asset (also known as a distributed energy resource or DER) connects to the grid and sells its surplus back to the grid for cash. In theory, there are people out there doing this who are making money off the generation and use of electricity! DERs are another area of interest that I plan to dive into for my next piece, so stay tuned there.

Market & Structure

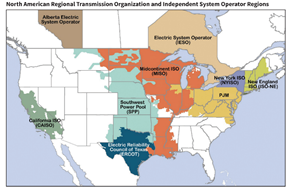

The market for electricity breaks down into B2B and B2C components. Wholesale markets are where utilities and traders transact (B2B) and retail markets are where utilities sell to consumers (B2C), and both markets, though separate, heavily influence each other. FERC determines what pricing rules the wholesale market will be subject to, options for which include a cost-based approach (setting the price some % above cost to produce) and a more laissez-faire approach based on supply and demand curves. Wholesale market has shifted in the direction of market-based pricing over the last few years. Outside of the wholesale market, independent system operators (ISOs) and regional transmission organizations (RTOs) introduce a competitive element to electricity markets and act as the connective tissue between wholesale energy producers and downstream actors. ISOs and RTOs are conceptually the same thing, so I will refer to them collectively as ISO/RTO through the remainder of this piece.

ISO/RTOs operate electricity transmission infrastructure independently of the wholesale market and create a competitive market for electricity by effectively acting as the middleman between wholesale markets and consumers. Since they own and operate the transmission lines, ISO/RTOs are well-positioned to incentivize electricity producers to offer the market the lowest possible price to ensure the electricity they generate is purchased and utilized. ISO/RTOs are just the middleman through which any actor can sell or bid for electricity generation, and in the US over 60% of the population is served by ISO/RTOs (see map to the left).

Electricity supplied to the market arrives in one of three ways: self-supply, through bilateral market purchases, or through spot purchases from RTO / ISO markets. Self-supply is relatively straightforward — an electricity provider generates power from an asset that it owns or operates. Bilateral purchases involve the electricity provider (the ultimate entity servicing the demand load) purchasing electricity from a third-party supplier. These transactions occur directly between two parties or over an exchange like the Intercontinental Exchange (ICE); trades over ICE tend to be more standardized while direct peer-to-peer transactions are more customizable (similar to the difference between options and forward contracts in the world of trading). Outside of the actual energy trade, there are a range of derivative trades the involved actors can make to de-risk the transaction and provide greater transparency to the broader market on future prices. Lastly, spot purchases from ISO/RTO markets involve an end provider purchasing the load they need to serve from an ISO/RTO marketplace. Typically, an end provider will use some combination of these acquisition mechanisms to serve load demand. I think there’s probably a lot of room for greater securitization / financialization in a lot of these markets as well as room for new types of insurance products that can be sold to market actors to help hedge swings in prices.

Grid Innovation

As mentioned previously, I highly recommend checking out The Grid: The Fraying Wires Between Americans and Our Energy Future by Gretchen Bakke, PhD for an excellent anthropomorphic accounting of the grid and how we arrived at today’s technology. Our current grid technology is aging, vulnerable to extreme weather, and its current state is considered a national security risk by the federal government. While there is plenty for policy to do here, I’d like to focus on the private sector innovation on the grid and how it may impact the decarbonization of electrification.

First up is growing the amount of utility-scale energy storage available to the grid today. Intermittent energy resources like solar and wind require large-scale storage to absorb spillover generation above and beyond what’s demanded at a given time (i.e. in the Pacific Northwest when it’s stormy, and both the wind and hydropower assets in the Columbia River Gorge generate supply far beyond what is demanded). If enough of this intermittent energy can be stored over the long-term and deployed when demand exceeds available supply, intermittent renewable sources of energy could over time become quasi-baseload energy resources. This would displace coal and natural gas, which currently act as baseload energy for the grid, and meaningfully advance the mission of decarbonizing the grid. I’ve written a bit about this topic here and am curious to hear about any companies in this space developing cool, non-Lithium ion related technologies to address this challenge.

Second up is expanding access to more advanced forms of net metering. Net metering integrated with all electricity-related entities in a home or work environment — like thermostats, home appliances, lighting, car chargers, solar panels, and more — could provide real-time usage data to electricity suppliers. Data at this scale would likely help electricity providers improve their predictive models for demand quite a lot, which reduces the chances of blackouts and grid failure. This massive increase in data coupled with AI applications could seriously improve the ability of models to accurately predict load shape and line up supply to meet it, thereby reducing risk and improving reliability of the grid. A precursor to advanced net metering and growing connectivity of the home is a general trend towards decentralization and, with it, distributed energy resources (DERs). In my next blog, I plan to do a deep dive into DERs and grid decentralization and what that might look like. I hope you will stay with me until then, and as always, please Tweet me @thegreengraham or email me at theexistentialinvestor@gmail.com with comments.

[1] This is Water, David Foster Wallace. http://metastatic.org/text/This%20is%20Water.pdf